Insurers are going through important losses from the catastrophic Los Angeles wildfires — given the excessive worth of houses and companies within the affected communities. Nevertheless, these losses are more likely to be manageable for each insurers and their reinsurers, with preliminary estimates starting from $10 billion to $15 billion, in keeping with S&P International Scores.

“Important wildfire losses within the first two weeks of 2025 may quickly deplete the disaster budgets of U.S. main insurers. This early pressure might result in earnings stress later within the yr, particularly if 2025 proves to be above-average for catastrophes,” S&P stated in its report, titled “Insurers Can Take in Losses Amid Escalating Los Angeles Wildfires.”

“Though anticipated losses are steep, we consider a lot of our rated insurers have the capital resilience to soak up them, after robust leads to the primary 9 months of 2024 (and sure for the yr),” S&P continued. “Furthermore, many main main insurers within the admitted market, akin to State Farm Mutual, Vehicle Insurance coverage Co., Allstate Corp., and Hartford Monetary Companies Group Inc., have both diminished publicity to or exited the California householders insurance coverage market over the previous two years.”

S&P doesn’t count on the LA wildfires to set off ranking modifications.

In its report on the LA wildfires, Moody’s Scores defined that after the key wildfires of 2017-2018, many California householders insurers nonrenewed insurance policies, “significantly in wildland-urban interface (WUI) areas, whereas enhancing underwriting requirements, conducting inspections, requiring householders to take steps to cut back wildfire threat and decreasing geographic clustering.”

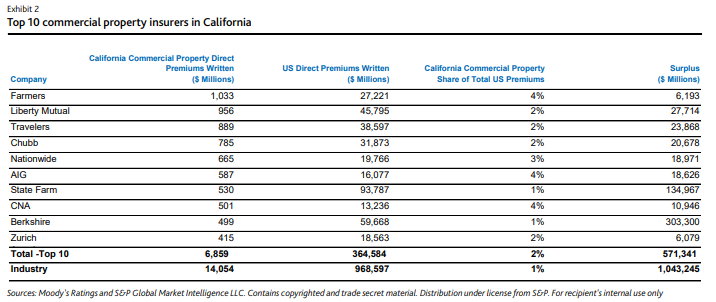

For the nonadmitted sector, S&P stated, the $3.6 billion written within the extra and surplus (E&S) property market in California is comparatively small. “These E&S specialty insurers are usually extremely diversified and might shortly increase premiums to recuperate

losses.”

Reinsurance Impression

On the identical time, S&P stated the impression on its rated international reinsurers can even be manageable “with no important impact on earnings because of the occasion’s magnitude and timing.”

The wildfire represents the primary main pure disaster loss within the yr for the sector and losses are more likely to will keep inside reinsurers’ pure disaster budgets for the primary quarter of 2025, S&P stated. “Nevertheless, it’s nonetheless unclear how mixture reinsurance protection could possibly be affected, given this can depend upon developments over the rest of the yr.”

Reinsurers are getting into 2025 with sturdy capitalization that’s supported by robust earnings in 2023 and 2024, “which helped the trade’s returns to exceed its value of capital,” S&P stated.

“The reinsurance sector stays disciplined concerning its urge for food for frequency losses, sustaining excessive attachment factors for protection,” the rankings company stated, noting that, regardless of selective value decreases throughout the January renewals, the sector remained dedicated to defending phrases and situations and people increased attachments.

Greater Attachments

There’s no query that this occasion will impression reinsurers – however at a manageable stage, commented economist Robert Hartwig, a scientific affiliate professor of finance and insurance coverage on the College of South Carolina, and head of the college’s Danger and Uncertainty Administration Heart, in an interview.

This wildfire occasion is extremely concentrated, geographically, and is extremely concentrated by way of the timeframe, which is “exactly what reinsurance is designed for,” he stated. “So it’s the kind of occasion that’s more likely to penetrate into reinsurance – even with increased retentions – though not as a lot as previously when retentions have been decrease.”

Hartwig famous that there shall be a larger impact on reinsurers from an occasion of this magnitude than from a complete summer time’s value of extreme convective storm occasions, which add as much as the identical greenback quantity. “And in every a kind of instances, the impression on reinsurers would’ve been mitigated by the upper attachments.”

California Market in Temporary

Moody’s Scores stated that losses shall be shared amongst commonplace householders insurers, insurers specializing in high-value extra and surplus traces (E&S) householders insurance policies, the California FAIR Plan and business property insurers. “Reinsurers can even assume losses by quota share, per-risk and extra of loss contracts,” Moody’s stated in its report, titled “Insurers face massive losses from devastating Los Angeles wildfires.”

“The allocation of losses amongst insurers will depend upon their market share for the affected areas, which can differ from market share within the state,” Moody’s continued. “Insurers handle their wildfire exposures by geographic diversification, top quality reinsurance safety and stable capital bases.”

California’s FAIR Plan, the state’s insurer of final resort, has grown quickly in recent times for householders and companies which have been unable to acquire protection within the non-public market. Moody’s stated this was a scenario that was exacerbated when California householders insurers nonrenewed insurance policies after the key wildfires of 2017-2018.

Insurers nonetheless bear the prices from these insurance policies, stated Moody’s as a result of the FAIR Plan “is a syndicated hearth insurance coverage pool comprising P&C insurers licensed to put in writing enterprise in California.”

“Insurers are required to take part within the FAIR Plan losses in direct proportion to an organization’s market share. Pacific Palisades is California FAIR Plan’s fifth highest wildfire publicity focus, with about $5.9 billion of publicity,” the Moody’s report continued.

New Regulatory Regime

In a separate report, AM Finest famous that California recently implemented regulations that will enable the price of reinsurance to be a consider pricing, whereas additionally allowing using disaster fashions to account for mitigation efforts by householders, companies, and communities. AM Finest’s report is titled “Increasing California Wildfires Anticipated to Incur Massive Insured Losses.”

“[T]he threat of wildfire could be very excessive and really persistent and the effectiveness of this system in decreasing insured losses will boil all the way down to affordability and the provision of applicable protection,” AM Finest stated, noting that there could also be challenges with respect to affordability, relying on the magnitude of the loss.

Beforehand, California was the one state to dam using these elements in insurers’ pricing, however that modified in January 2025, stated Hartwig. “Insurers now shall be allowed to make use of forward-looking climate-based fashions and incorporate these of their charges. The quid professional quo is that insurers would start to put in writing once more within the state, or would increase their writings.”

Nevertheless, there may be basic concern that this occasion may doubtlessly set again the intent of the brand new regulatory regime, Hartwig stated, explaining that that is going to be one of the expensive fires in California historical past, and it’s simply the second week of January.

Insurers might find yourself submitting for fee will increase for householders and business property renewals, efficient in 2026, which can be bigger than what had been anticipated, he added.

Moody’s acknowledged that it’ll take time to find out how this laws and the pending wildfire losses will have an effect on the California householders insurance coverage market.

S&P stated the LA wildfires doubtlessly evaluate with insured losses skilled within the North California wildfires of 2017 (Tubbs Hearth) and in 2018 (Camp Hearth), which value the trade practically $16 billion and $14 billion, respectively.

The conundrum for insurers is that the January fires are occurring throughout what needs to be the California’s wet season, Hartwig stated. “Basically, the wildfire season of 2024 by no means ended.”

“Winter is usually the wet season for Southern California, which makes wildfires in January comparatively uncommon,” Moody’s stated. “Nevertheless, this winter has been unusually dry. Efforts to combat the Palisades wildfire have reportedly been stymied by restricted water provide and low stress for hearth hydrants.”

(Editor’s be aware: Moody’s stated its evaluation comes from Moody’s Scores credit standing company, and doesn’t symbolize Moody’s official estimates for insured losses, or for financial losses/property harm. These estimates, which aren’t supplied by the rankings company, shall be shared by Moody’s at a later date.)

Water is dropped by helicopter on the burning Sundown Hearth within the Hollywood Hills part of Los Angeles, Wednesday, Jan. 8, 2025. (AP Picture/Ethan Swope)

Associated:

Matters

Catastrophe

Natural Disasters

Profit Loss

Wildfire

Louisiana

Reinsurance

{kind=link}