The work that GEICO’s chief govt has executed to “repolish” Berkshire Hathaway’s “long-held gem” bought a particular shout-out in Warren Buffett’s Berkshire Hathaway 2024 annual report back to shareholders final weekend.

GEICO’s $4 billion-plus leap in 2024 underwriting revenue (earlier than taxes) versus 2023, and one other $5 billion enhance in funding earnings throughout all of Berkshire’s insurance coverage operations in comparison with 2023, defined the majority of the conglomerate’s enchancment in working earnings.

Berkshire’s whole working earnings of $47.4 billion after taxes was $10 billion increased than working earnings for 2023—up by 27% on a share foundation.

“In 2024, Berkshire did higher than I anticipated, although 53% of our 189 working companies reported a decline in earnings,” Buffett wrote in his annual letter opening the report.

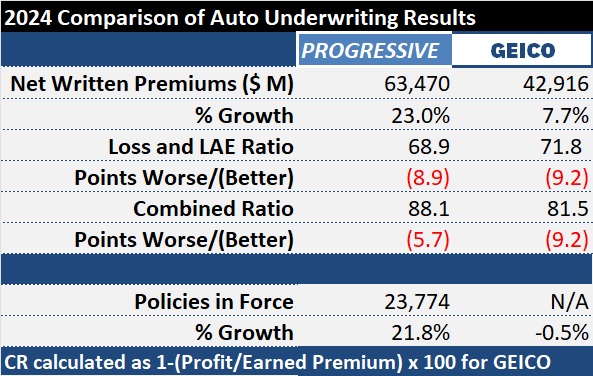

GEICO was one among Berkshire’s companies that recorded elevated earnings final yr. Underwriting revenue earlier than taxes of $7.8 billion was greater than double $3.6 billion posted in 2023—and a reversal of an almost $2 billion underwriting loss recorded for 2022.

“In 5 years, [CEO] Todd Combs has reshaped GEICO in a serious method, growing effectivity and bringing underwriting practices updated,” Buffett wrote. “GEICO was a long-held gem that wanted main repolishing, and Todd has labored tirelessly in getting the job executed. Although not but full, the 2024 enchancment was spectacular,” he wrote.

GEICO’s mixed ratio landed at 81.5 for 2024—9.2 factors higher than 2023 and greater than 20 factors higher than 2022.

The Administration’s Dialogue and Evaluation (MD&A) part of the report attributes GEICO’s 2024 enchancment in pretax underwriting earnings to increased common premiums per coverage and “improved working efficiencies.”

The working efficiencies, nonetheless, didn’t affect the expense ratio in 2024. The expense ratio didn’t budge—remaining at 9.7 in 2024 and 2023—whereas the loss and loss adjustment expense ratio improved to 71.8. In 2023, a part of the mixed ratio enchancment got here from a 2.0 level drop in GEICO’s expense ratio.

Whereas GEICO didn’t reduce employees as sharply in 2024 because it did in 2023, the newest staffing determine for the private auto insurer stands at 28,247—a stage that’s now under the worker rely GEICO reported method again in 2013. The variety of workers at GEICO is now 33% decrease than its excessive level of 42,156, recorded 5 years in the past in 2020.

GEICO’s policies-in-force continued to fall in 2024—however solely barely. The MD&A reveals the 2024 PIF rely was 0.5% decrease than the year-end 2023 PIF. Within the 2023 annual report, GEICO had reported nearly a ten% drop in policies-in-force.

The speed of decline in policies-in-force slowed within the first half of 2024, after which the variety of insurance policies grew within the second half of the yr. Nonetheless, the general decline for the yr stands in distinction to competitor Progressive, which noticed insurance policies and web written premium each develop greater than 20% in 2024.

No ‘Monster’ Occasion; Prior-Yr Legal responsibility Reserves

Commenting on the property/casualty insurance coverage companies typically, Buffett famous “insurance coverage pricing strengthened throughout 2024, reflecting a serious improve in injury from convective storms.”

“Local weather change could have been saying its arrival,” he stated. “Nevertheless, no ‘monster’ occasion occurred throughout 2024. Sometime, any day, a really staggering insurance coverage loss will happen—and there’s no assure that there will likely be just one every year.”

Though they didn’t affect Berkshire’s 2024 earnings, the corporate estimated losses of $1.3 billion from the California wildfires in January.

In 2024, GEICO’s outcomes had been impacted by $360 million in losses associated to Hurricanes Helene and Milton. Berkshire’s different main insurance coverage operations incurred $350 million of disaster losses, and the reinsurance operations recorded $800 million in cat losses.

“We aren’t deterred by the dramatic and rising loss funds sustained by our actions. (As I write this, suppose wildfires.) It’s our job to cost to soak up these and unemotionally take our lumps when surprises develop,” Buffett wrote in his letter.

“It’s additionally our job to contest ‘runaway’ verdicts, spurious litigation and outright fraudulent conduct,” he wrote, referring to the impacts of social inflation.

This yr’s annual report included a extra direct reference to social inflation in administration’s dialogue of the outcomes of Berkshire Hathaway Major Group—the one one of many three main P/C divisions (GEICO, Berkshire Hathaway Major Group and Berkshire Hathaway Reinsurance Group) to report decrease underwriting earnings in 2024 than in 2023.

Regardless of recording highest top-line premium development among the many three segments, the report defined a 2.1-point improve in BH Major’s loss and LAE ratio partially displays a decrease stage of takedowns for prior accident years’ claims—nearly $0.5 billion decrease than BH Major recorded in 2023.

“The comparative decline mirrored a major improve in loss estimates at GUARD and decrease reductions in estimated losses throughout a number of of our different companies that write medical skilled legal responsibility and industrial legal responsibility coverages, partially offset by elevated reductions of property loss estimates.”

“Throughout 2024, attributable to deteriorating loss expertise, administration at GUARD carried out a complete overview of claims and considerably elevated estimated final declare liabilities,” the report says, including that for different companies in BH Major Group, decrease quantities of favorable growth associated to prior years’ legal responsibility claims “was attributable to unfavorable social inflation traits, together with the impacts of jury awards and litigation prices.”

Nonetheless, Buffett stays bullish on Berkshire’s insurance coverage and reinsurance companies. “All issues thought-about, we just like the P/C insurance coverage enterprise. Berkshire can financially and psychologically deal with excessive losses with out blinking,” he wrote. “We’re additionally not depending on reinsurers and that provides us a fabric and enduring price benefit,” he famous.

Berkshire’s personal P/C reinsurance operations recorded $3.8 billion of underwriting earnings in 2024, with retroactive reinsurance posting $0.9 billion of underwriting losses. P/C reinsurance written premiums declined 2.1% to $21.9 billion, whereas earned premiums grew 1.4%. The report discloses a cost of virtually $0.5 billion recorded by the group’s Nationwide Indemnity Firm associated to a settlement settlement of a non-insurance affiliate that filed for chapter, which impacted underwriting bills.

Featured photographs: AI-generated (Adobe/Firefly)

Q1 2025 Earnings Name Transcript")

{kind=link}