Floods

Extra Personal Insurers Writing Flood Protection; Shopper Demand Continues to Lag

Jeff Dunsavage, Senior Analysis Analyst, Triple-I (08/17/2023)

Flood is now not an “untouchable” threat for personal insurers, in response to a brand new Triple-I “State of the Danger” Issues Brief. Actually, information suggests insurers see flood threat as a rising space of alternative. That’s excellent news for owners who perceive the evolving nature of the peril.

For many years, FEMA’s Nationwide Flood Insurance coverage Program (NFIP) was virtually the one accessible choice for owners searching for flood protection. Improved information, evaluation, and modeling have helped drive elevated private-sector curiosity in flood-risk switch and mitigation.

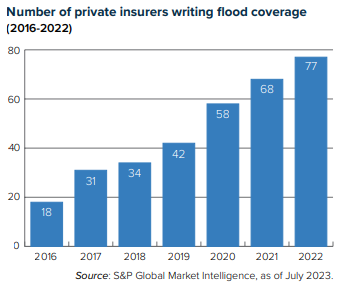

Since 2016, when solely 12.6 % of flood protection was written by 18 personal insurers, the market has grown considerably. In 2022, the whole flood market had grown 24 % – from $3.29 billion in direct premiums written (DPW) in 2016 to $4.09 billion – with 77 firms writing 32.1 % of the enterprise.

The timing of the personal market’s rising urge for food for flood threat is fortuitous, because it coincides with Risk Rating 2.0, NFIP’s new pricing methodology that goals to make the federal government company’s flood insurance coverage premium charges extra actuarially sound and equitable by higher aligning them with particular person properties’ flood threat. As NFIP charges change into extra aligned with ideas of risk-based pricing, some policyholders’ costs are anticipated to fall, whereas many are going to rise.

It’s cheap to count on that, as the price of collaborating within the government-run flood insurance coverage program rises for some, personal insurers will acknowledge the market alternative and reply by making use of cutting-edge information and analytics capabilities, extra refined pricing strategies, and new merchandise, akin to parametric insurance, to grab these alternatives. It is also incumbent upon communities to discover modern approaches like community-based disaster insurance packages.

Sadly, as risk-management agency Milliman points out, “A relative lack of shopper demand in comparison with different property insurance coverage choices nonetheless provides carriers hesitation when making an attempt to judge whether or not they need to spend money on launching their very own personal flood packages.”

Public schooling and consciousness constructing round flood threat are important to advance the objective of decreasing flood threat, as is collective motion amongst stakeholder teams – from banks and insurers to group leaders, actual property professionals, and policymakers. Decreasing the specter of pricey flood claims might be needed to make sure that reasonably priced insurance coverage safety is out there to all who want it.

Triple-I collaborates with its insurer members, different nonprofits, insurtechs, and different companions to advertise pre-emptive mitigation and fast restoration to learn policyholders, insurers, communities, and companies. Its Resilience Accelerator gives entry to instruments and sources, together with flood peril maps and webinars that includes leaders in threat and insurance coverage innovation.

Study Extra:

Stemming a Rising Tide: How Insurers Can Close the Flood Protection Gap

Climate Risk Isn’t All About Climate: Population, Land Use, Incentives Need to Be Addressed

Coastal Virginia Rises to Meet the Challenge of Sea-Level Rise

{kind=link}