Many have been there watching a staff’ compensation insurance coverage proposal, overwhelmed by a premium so steep it looks like a punishment. The reason appears easy: one massive, catastrophic declare has thrown your expertise modification issue (EMOD) into chaos, leaving you with an astronomical invoice.

However right here’s the factor—this clarification isn’t simply oversimplified; it’s mistaken. In actuality, a single declare virtually by no means causes the form of spike that sends premiums into orbit. The true story lies within the math, and understanding it may possibly save your online business from falling right into a pricey entice.

The Math

Opposite to widespread perception, the EMOD system is designed to keep away from catastrophic fluctuations attributable to remoted incidents. Listed below are the three key components that guarantee stability:

- The Stabilizing Worth: The stabilizing worth is a numeric worth discovered on the underside a part of an EMOD calculation. Aptly named, it acts as a ballast. It stays the identical on each the numerator and denominator sides of the equation. Its goal is to maintain issues in verify and forestall singular claims from massively fluctuating or influencing an EMOD on their very own. It additionally ensures that any given firm has an EMOD, even when there aren’t any claims.

- The W Issue (Weighting Issue): That is an additional low cost given to claims that exceed the cut up level for any singular declare and change into an extra declare. The W issue is a major low cost that usually ranges from 95% to 60%, relying on the dimensions of the corporate. It’s used to considerably cut back the influence a large declare has on any given enterprise.

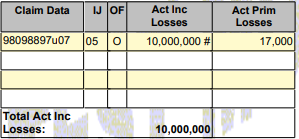

- Whole Declare Cap: The entire declare cap serves as the utmost quantity of declare {dollars} that can influence an EMOD rating. This varies by state and is up to date yearly, however its perform by no means adjustments. As soon as this restrict is reached, a pound signal will seem subsequent to the overall greenback quantity. This means that this declare has reached its max, that means that solely the cash as much as the cap restrict will have an effect on the EMOD rating. So how a few declare that’s $500,000, $1,000,000, or $10,000,000? It doesn’t make a distinction; solely the quantity as much as the cap quantity will rely within the EMOD calculation.

This framework, established by the Nationwide Council on Compensation Insurance coverage (NCCI), ensures that even giant, uncommon claims have a restricted impact in your EMOD. Because the NCCI states, “One very giant loss doesn’t indicate a sample of declare frequency.”

The true driver of excessive EMOD scores isn’t the one-in-a-million declare—it’s the small, frequent, and sometimes missed claims. These recurring incidents, when mismanaged, add up over time and weigh closely on the EMOD calculation. A single catastrophic declare is much less predictive of future threat than a sample of frequent, smaller claims. It’s these smaller claims that exhibit an absence of efficient threat administration and drive premiums increased.

In uncommon instances, a single declare may cause a major EMOD hike—however just for small companies with minimal anticipated losses. For instance, an accounting agency with a modest staff’ comp coverage may see its EMOD spike following a extreme automobile accident involving its staff. Even then, the precise premium improve can be marginal for an organization that has a small premium base to start with.

Whereas it could be tempting to attribute an elevated EMOD to a single declare, that is hardly ever the case. It’s a simplistic and handy strategy to sidestep the extra complicated actuality: excessive EMODs usually outcome from quite a few mismanaged small losses. This shifts the accountability for EMOD management again to the corporate and the dealer. The important thing to sustaining a low EMOD lies in successfully managing small and frequent claims, relatively than merely hoping {that a} main declare received’t influence you. Essentially the most regarding claims often aren’t the memorable ones however people who slip below the radar—unnoticed and unattended—resulting in persistently excessive EMODs. These missed claims are the place the actual destructive shifts happen, however in addition they current vital alternatives. By addressing these claims, an organization can take management of their EMOD and, consequently, the premiums they pay.

Subsequent time somebody tells you, “It’s all due to that one unhealthy declare,” you’ll be able to confidently reply: “It’s not that straightforward.” The reality lies within the math, and the maths doesn’t lie. Managing your EMOD means managing the small, frequent claims that fly below the radar—not fearing the occasional massive one.

The facility to decrease your staff’ comp premium isn’t in avoiding unhealthy luck—it’s in making smarter selections. And that’s not simply math; that’s empowerment.

For additional building and threat administration assets, contact INSURICA as we speak.

This isn’t meant to be exhaustive nor ought to any dialogue or opinions be construed as authorized recommendation. Readers ought to contact authorized counsel or an insurance coverage skilled for applicable recommendation.

{kind=link}