The tariff shock and recession fears which have despatched world shares right into a tailspin over the past week are rolling into company funding markets, elevating the price of borrowing and disrupting financing plans even for lower-risk corporations.

With U.S. Treasuries nursing large losses on Wednesday – the strongest signal but that stress is impacting so-called safe-haven belongings – consideration has now turned to the $35 trillion international company bond market, which has swelled by round 40% since 2008 as corporations gorged on low cost debt, OECD data show.

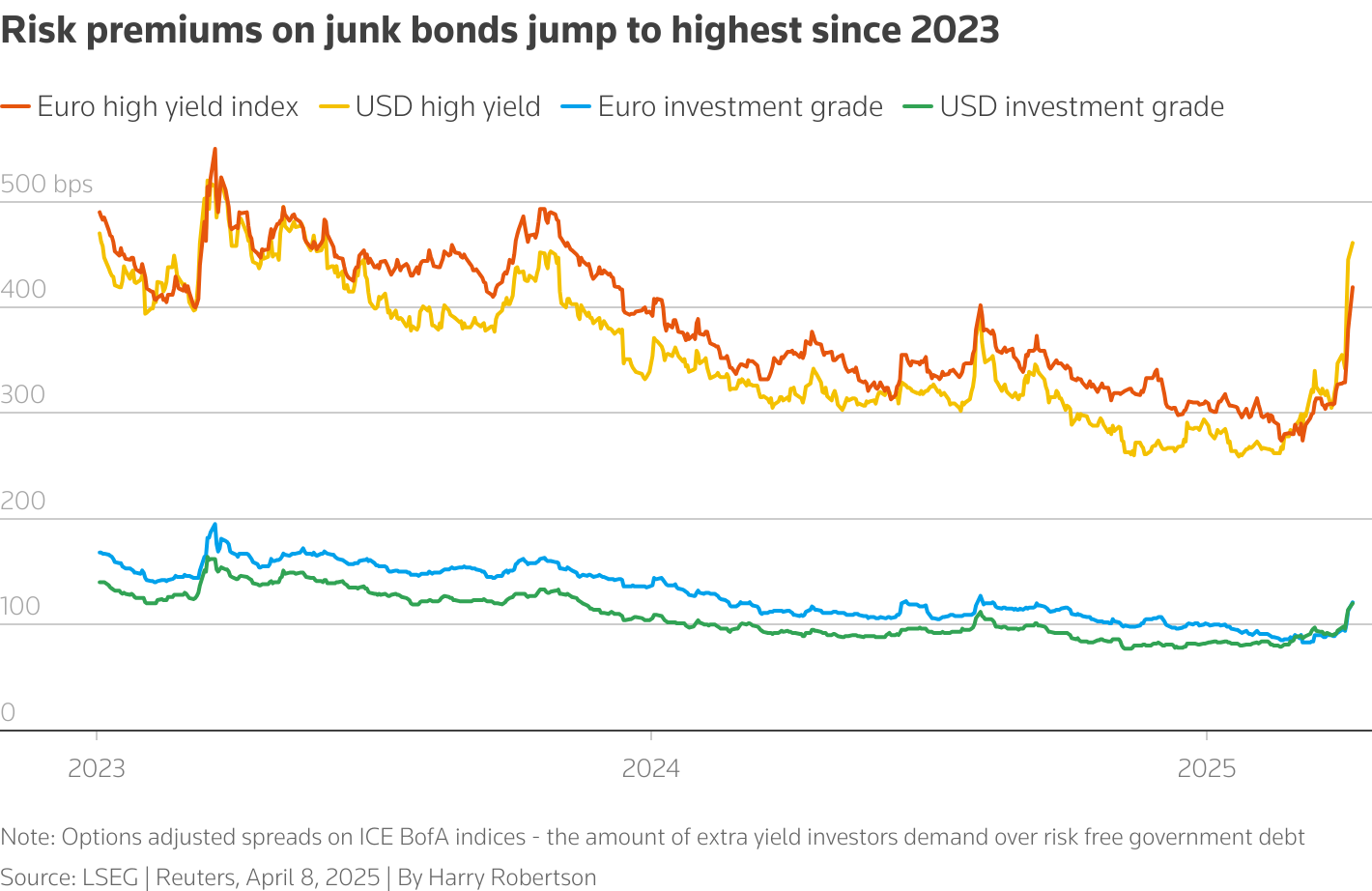

The premium traders demand to carry low-rated company credit score .MERHW00 versus authorities debt has soared by 100 foundation factors in per week, the largest short-term transfer in so-called international junk bond spreads for the reason that U.S. regional banking disaster in March 2023.

Associated article: Global Credit Starts to Wobble as Market Pain Spreads

The transfer is fueling fears pension funds and different longer-term traders may additionally begin purging higher-quality debtors from their portfolios. With the vast majority of fixed-income buying and selling taking place off-market, it may be exhausting to trace and measure gross sales.

However the sharp dip in sentiment is much simpler to discern. An index measuring the price of insuring towards debt defaults by Europe’s strongest companies hit its highest since late 2023 ITEEU5Y=MP on Wednesday.

Germany vitality group RWE, which has an funding grade ranking, was amongst corporations which were affected by the turmoil. Regardless that it employed banks to difficulty a inexperienced bond final month, it was unable to launch the sale amid the tariff information and ensuing market volatility, two folks aware of the matter mentioned. RWE declined to remark.

In Japan, three corporations have postponed the sale of 100 billion yen ($680 million) price of yen-denominated bonds this week.

For some traders, it’s a query of when contagion grips, reasonably than if.

“What you possibly can clearly observe is that liquidity on the credit score aspect has dried up,” Lazard Asset Administration international fastened earnings co-head Michael Weidner mentioned.

“Liquidity and buying and selling exercise grinds to a halt first in mortgage and high-yield markets after which strikes over to IG (funding grade) credit score.”

No Funding Grade Disaster, But

For now, most traders and analysts are predicting higher ructions within the high-yield market, which is populated by corporations with heavy debt burdens, patchy earnings profiles and prospects broadly considered as most in danger from recession.

Aberdeen funding grade credit score director Luke Hickmore mentioned he noticed few indicators of panic amongst traders in lower-risk debt securities, whereas credit score strategists at UBS have informed shoppers the present state of affairs in credit score markets was “nowhere near absolutely the worst case.”

Chris Arcari, head of capital markets at monetary companies and pension fund marketing consultant Hymans Robertson, was to date sanguine in regards to the strikes.

“We’re coming from a place the place spreads have been very, very tight following loads of yield pushed demand,” he informed Reuters.

“I don’t see any large contagion. I feel there’s a rational repricing if that is smart. It’s not catastrophe stations.”

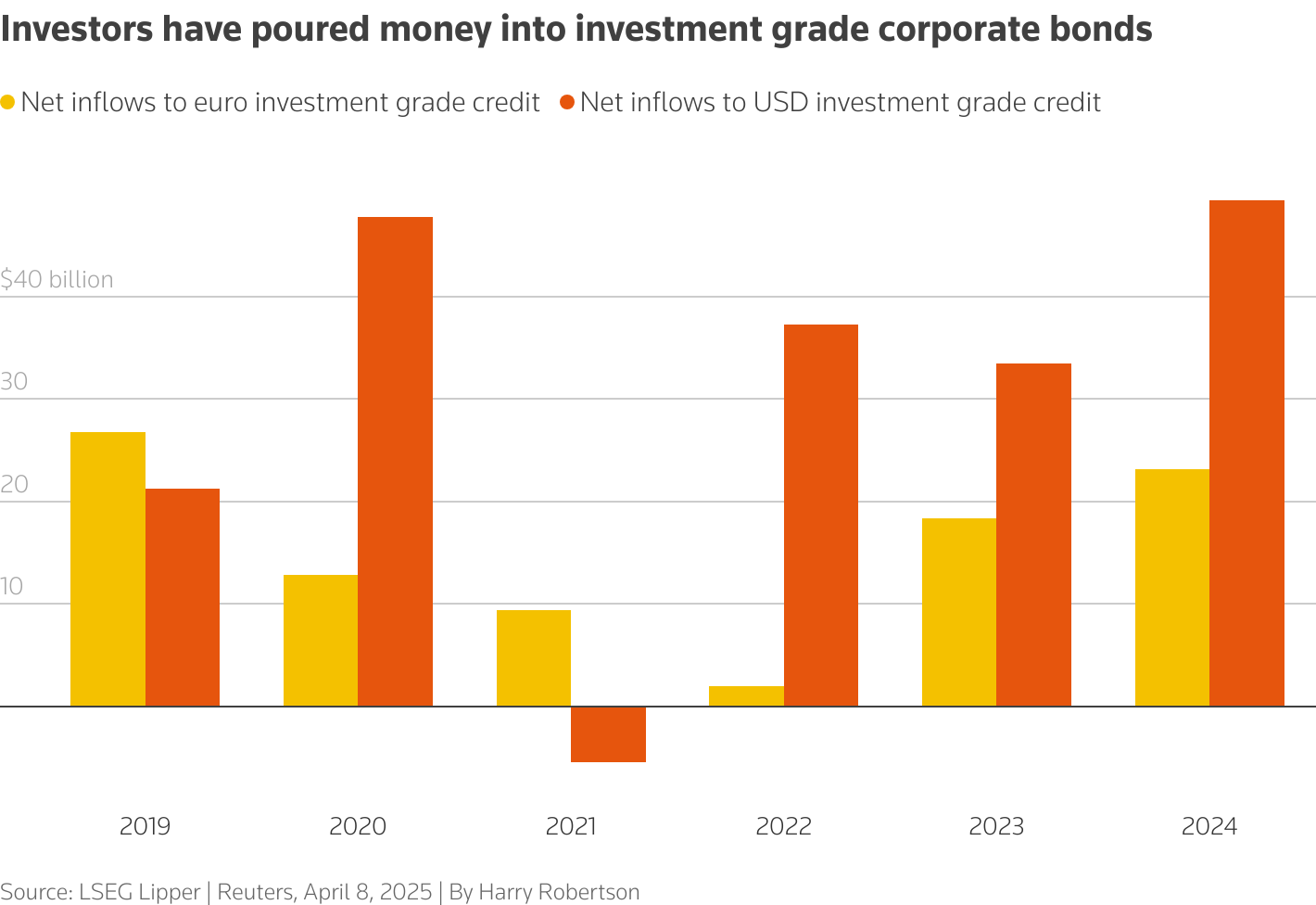

Buyers pumped document sums into U.S. dollar-denominated funding grade debt funds final 12 months, in keeping with knowledge from LSEG Lipper. For euro-denominated funds, inflows have been the largest since 2019.

A part of internet outflows from these funds – and a selloff in among the names most delicate to a commerce battle – was more and more possible, analysts mentioned, significantly after the primary post-tariff knowledge is printed.

Edmond de Rothschild Asset Administration head of multi-asset Michael Nizard, who mentioned he began backing out of high-yield debt in late March, added that cash managers have been additionally prone to be promoting funding grade debt to shore up money reserves.

“They face outflows from shoppers and so they should promote for money,” he mentioned, predicting a “new spherical” of credit score spreads widening within the brief time period.

However investment-grade defaults have been uncommon even in the course of the pandemic, which outdoors the 2 world wars, represented the best “financial full cease in fashionable instances,” Aberdeen’s Hickmore mentioned.

Citi strategists famous on Tuesday that the darkening credit score outlook had pushed pricing of three just lately issued high-yield bonds past 10 proportion factors over the risk-free price.

In a pessimistic situation the place high-yield spreads proceed to widen sharply, Sharon Ou, vp and senior credit score officer at Moody’s Rankings, mentioned the worldwide default price might exceed 8% in a 12 months’s time from lower than 5% as we speak.

“The market dynamics have modified within the sense that this isn’t purely about who’s uncovered to tariffs or not, this can be a large detrimental shock for the general economic system, and that impacts everybody,” mentioned Viktor Hjort, head of credit score analysis at BNP Paribas.

“However have we seen a panic occasion? Nothing near what we noticed in 2022.”

Dangers for Funding Grade Rising

Buyers mentioned solely a rollback of tariffs by the White Home or central financial institution price cuts might insulate credit score markets from right here.

RW Baird strategist Ross Mayfield mentioned he nonetheless favored high-quality corporations’ debt, however dangers for funding grade have been rising, with even a U-turn by Trump on tariffs probably including to market and enterprise uncertainty as a substitute of rebuilding confidence.

And even when the Fed does lower charges to assuage roiled markets, aid for corporations could possibly be short-lived.

Based on the OECD, on the finish of 2024, 63% of funding grade debt and 74% of non-investment grade debt had curiosity prices beneath the prevailing market charges and most will possible require refinancing at the next value.

“In a stagflationary setting from tariffs, you’ll see each funding grade and excessive yield company debtors battle as their prices of debt rise,” Mayfield mentioned.

(Writing by Sinead Cruise; extra reporting Emma-Victoria Farr and Anousha Sakoui; modifying by Amanda Cooper and Hugh Lawson)

{kind=link}