S&P World Market Intelligence is forecasting a mixed ratio of 99.2 for the U.S. P/C insurance coverage business general in 2024, signifying a return to underwriting profitability for the primary time since 2021.

In line with the evaluation, non-public passenger auto insurance coverage is anticipated “to make a dramatic return to underwriting profitability,” with S&P GMI projecting a private auto 2024 mixed ratio of 98.4, down from 104.9 in 2023 and 112.2 in 2022. With private auto representing virtually 35 p.c of general P/C insurance coverage business premiums written, that turnaround is what’s going to drive the general underwriting revenue for the business, in keeping with S&P GMI projections offered within the “S&P World Market Intelligence 2024 U.S. P&C Insurance coverage Market Report” printed late final week.

The mixed ratio for the business general will drop 2.5 factors to 99.2 from a degree of 101.7 in 2023, and enhance a bit extra to 99.0 in 2025, the report exhibits.

S&P GMI’s forecast that industrywide underwriting outcomes can be again within the black this 12 months contrasts projections from analysts on the Insurance coverage Info Institute and Milliman. They point out that the business will report one other general underwriting loss—and an underwriting loss within the private auto line—in 2024, with restoration not anticipated till 2025.

Associated: P/C Premium Growth Likely But Profits Delayed Until 2025: Forecast

With owners outcomes lagging behind private auto, S&P GMI shouldn’t be anticipating that the non-public traces phase general will report an underwriting revenue this 12 months or subsequent 12 months. The private traces mixed ratio will come near breakeven in 2026, in keeping with the five-year projections offered by line and phase within the report. The projected private traces mixed ratios are 101.2 for 2024 and 100.2 for 2025, in comparison with 106.7 in 2023.

Climate catastrophes proceed to weigh on the owners enterprise, and though the report notes (in a piece outlining the methodology) that S&P GMI assumes a traditional disaster load for uncovered enterprise traces, for owners, the mixed ratio continues to be pegged at an unfavorable 107.3 for 2024. That’s down from 110.9 in 2023, which had been the worst end in a dozen years.

For private traces insurers, outcomes may also proceed to be uneven as mutuals and reciprocals want greater than charge hikes to get well from challenges to auto and owners traces in recent times, the report says. (Mentioned additional beneath.)

The industrial traces phase will stay worthwhile all through the five-year projection interval, though charts within the report reveal that the projected 2024 industrial traces mixed ratio of 96.0 will creep as much as 98.2 by 2028.

The very best mixed ratio projection for the U.S. P/C insurance coverage business general can also be indicated for the final 12 months of the forecast interval—99.9 for 2028—with underwriting outcomes remaining within the black all through the five-year timeframe.

The report calls out a “faster-than-expected erosion” in staff compensation outcomes as essentially the most vital danger to S&P GMI’s industrial traces outlook for continued underwriting profitability.

Commenting on drivers of earnings past underwriting revenue, the S&P GMI report notes that “the business stands to learn materially from increased rates of interest” after years and years of web yields on invested belongings coming in at report low ranges.

“The business’s ongoing effort to rotate into high-quality, higher-yielding belongings will function a catalyst for progress in web earnings even to the extent that underwriting margins stay comparatively modest,” the report says.

“A key variable would be the business’s continued adherence to disciplined underwriting in a extra forgiving funding panorama,” the report says.

High Line Development Set to Drop

On the highest line, S&P GMI initiatives a remaining 12 months of double-digit industrywide progress in 2024, with premiums throughout all traces leaping 10 p.c for full-year 2024 however then falling to five.9 p.c or decrease in 2025-2028.

“A considerable decline within the tempo of will increase in non-public auto premium volumes serves as the first contributor to our projection that the speed of progress in U.S. P/C business direct premiums written will recede to the mid-single digits on an annual foundation from 2025 by means of 2028,” stated Tim Zawacki, insurance coverage sector strategist at S&P World Market Intelligence in a press release accompanying the report. Zawacki defined that the magnitude of the advance in underwriting outcomes is prone to immediate “pretty speedy retreats within the scope and scale” of the numerous private auto charge will increase pursued by most market individuals during the last three years.

In line with the report, S&P GMI’s RateWatch utility confirmed combination authorised charge modifications by means of the primary half of 2024 dropping to five.9 p.c, down from an “outsized full-year 2023 tally” of 15.2 p.c. Nonetheless, the speed hikes taking impact within the second half of 2023 have but to totally impression earnings statements by means of 2024, the report notes, including that charge momentum has endured within the different main private line: owners.

Whereas the report exhibits direct premium progress for all private traces hovering round 14 p.c for 2023 and 2024, and dropping to the 4-7 p.c vary within the subsequent 5 years, industrial traces progress charges have already fallen beneath double-digit ranges of 2021 and 2022. The projected industrial traces direct premium progress charge is 6.2 p.c for 2024, with progress charges thereafter within the 5-6 p.c vary.

Total, the ten p.c progress in direct premiums written throughout all traces marks the fourth straight 12 months for progress of 9.5 p.c or extra.

“The period of the enlargement is with out precedent in at the very least a technology because the earlier comparable hard-market cycle within the early a part of the twenty first Century had solely three years with annual progress charges of 9.5 p.c or extra,” the report notes.

Relative Efficiency

The report consists of line-by-line particulars for historic mixed ratio and progress charges going again to 2014 and projected ahead to 2028, together with aggregations for the non-public and industrial traces sector and the U.S. P/C insurance coverage business. For every line analyzed and for the segments, the report additionally presents charts displaying mixed ratios and premiums for the highest 15 gamers.

In non-public passenger auto, for instance, the report exhibits that solely Erie (ranked twelfth by 2023 premium) and CSAA (ranked 14th) posted worse mixed ratios than the most important private auto insurer, State Farm, in 2023. State Farm’s 115.3 mixed ratio towered over the ratios recorded for the second- and third-largest writers—Progressive and GEICO, coming in at 94.2 and 92.1, respectively. Erie Insurance coverage posted a 123.3 ratio and CSAA’s outcome was 117.1, in keeping with S&P GMI.

The report features a part dedicated to S&P GMI’s efficiency rankings—decided by S&P GMI analysts utilizing 13 monetary metrics from 2023 statutory filings to measure charges of return, steadiness sheet enlargement, funding efficiency and prior-accident-year reserve growth, along with underwriting profitability and premium progress. Industrial traces gamers dominate these rankings, however steadiness might return, with tailwinds benefiting private traces carriers whereas headwinds are already rising in sure elements of the industrial traces, Zawacki noticed in a recent article he wrote concerning the rankings for Provider Administration.

Analyzing relative premium progress charges for particular person carriers, S&P GMI exhibits that Tesla Insurance coverage was the most important sprinter with a triple-digit progress charge of almost 768 p.c placing direct and web written premiums at roughly $110 million.

Associated article: Tesla Insurance Blasts Off to Top P/C Insurance Growers Chart

Private v. Industrial; Inventory vs. Mutual

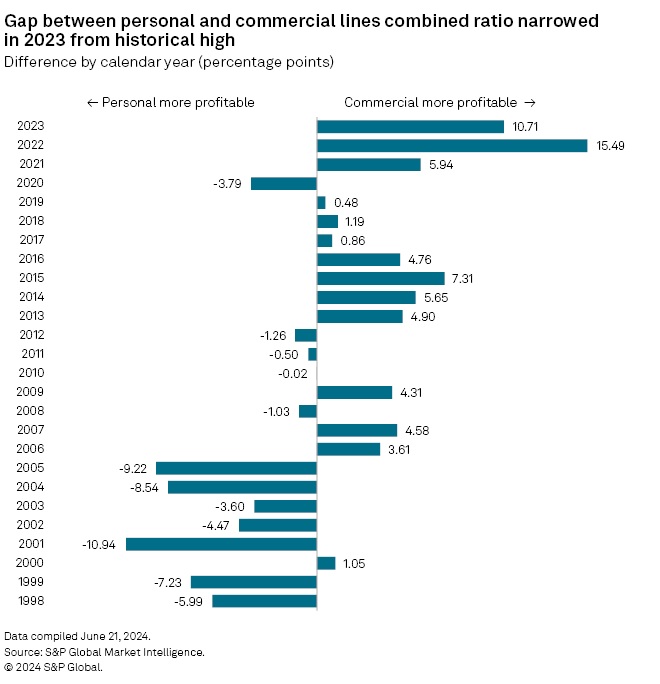

The S&P GMI report reveals clear contrasts in underwriting outcomes for industrial vs. private traces insurers. Aside from 2020, private traces underwriting outcomes haven’t bested industrial traces since 2012.

In 2023, the industrial phase mixed ratio was greater than 15 factors higher than private traces, with the distinction projected to slender to about 11 factors in 2024.

Bifurcating the business one other method—by possession construction—S&P GMI calculates a 107.9 cumulative mixed ratio for the 2021-2023 interval for mutuals, inventory insurers which can be a part of mutual insurance coverage holding firm constructions, and reciprocal exchanges (excluding policyholder dividends). That outcome was 11.3 share factors increased than the remainder of the business.

“Mutuals are usually extra concentrated within the embattled dwelling and auto enterprise than inventory insurers, conferring upon them the misfortune of experiencing the worst of the present cycle. However charge alone could also be inadequate for them to beat the depths of the challenges they face,” the report says.

Going ahead, S&P GMI’s outlook anticipates larger market-share focus among the many largest non-public auto writers within the coming years, reasoning that “information, analytics and economies of scale stay critically essential in a commoditized enterprise.”

For owners, in distinction, S&P expects extra market fragmentation as nationwide carriers trim again publicity to loss-prone markets.

The report additionally consists of evaluation of progress within the E&S market, together with premium rankings of E&S writers for owners and industrial property traces, drawing from a dialogue of market developments included in an earlier report, The 2024 US Excess & Surplus Market.

Subjects

Carriers

Auto

Profit Loss

Personal Auto

Underwriting

Property Casualty

{kind=link}