The auto insurance coverage trade has weathered its share of storms lately. Regardless of fewer claims in early 2024, carriers nonetheless face headwinds with regards to car complexity and its impact on severity and cycle time.

Following are the 4 most notable tendencies to observe in 2025 to assist your group efficiently navigate the street forward.

1. Complete Loss Frequency is Rising

For years, new automotive depreciation started as soon as a car was pushed off the lot. In actual fact, Kelley Blue Book reported that vehicles misplaced half their buy value throughout the first 5 years. Having a used car enhance in worth over time was not speculated to occur. However it did.

Extra lately, this development has begun to unwind, and car values at the moment are rightsizing. Within the U.S., for instance, CarGurus reported that used car costs fell 7.25% this summer season in comparison with final. In Canada, the tempo of depreciation—a 14.4% year-over-year lower—occurred extra quickly in accordance with Black Book.

Along with altering car economics, the vehicles on our roads are getting older. In 2002, the typical age of the automotive parc was practically 9 and a half years. In 2024, it elevated to a file 12.6 years within the U.S. Whereas the typical car in Canada is consistently two years newer, it has additionally trended older at the same charge. Consequently, the typical age of a repairable, collision-damaged car has risen as effectively (to six.94 years within the U.S. and 6.01 years in Canada).

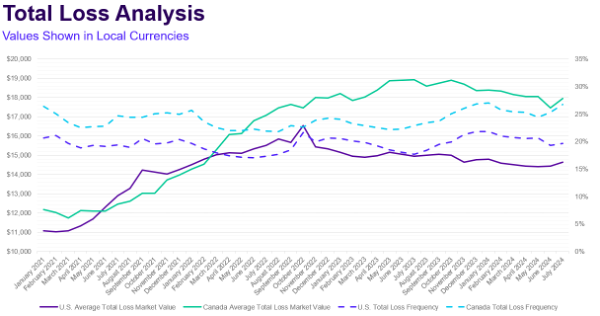

As car values drop and the demand for brand new vehicles lessens, whole loss frequency is growing and is anticipated to proceed its upward trajectory into 2025. Complete loss market values, alternatively, will possible return to the place they might have been traditionally if we didn’t have a large disruption throughout COVID. In actual fact, by Might 2025, the typical whole loss market worth is anticipated to be:

- 5% above historic common progress within the U. S.

- 13.2% above historic common progress in Canada

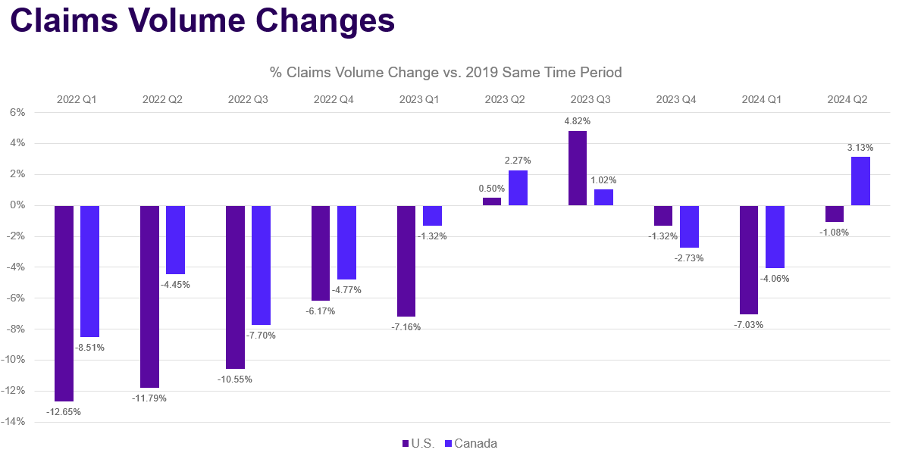

2. Claims Volumes Proceed to Fall

The lower in claims volumes was a scorching subject in early 2024. The questions now are what’s driving volumes down, will we see declines of seven% like we did within the U.S. earlier this yr as in comparison with 2019 and the pre-COVID period, and the way will that have an effect on insurance coverage underwriting choices and restore facility revenues?

Though many need to attribute the discount in claims to the rising availability of superior driver help programs (ADAS), the extra possible trigger was a light winter. With no snow and ice on the street, much less precipitation and hotter temperatures, there are fewer accidents.

Nevertheless, that’s not the entire story. Insurance coverage affordability can also be prompting customers to make totally different selections. For instance, to maintain auto insurance coverage payments from growing when premiums rise, policyholders might determine to vary their protection or elevate their deductible. In response to information from the U.S. Bureau of Labor Statistics, many have chosen the latter possibility.

Earlier than 2021, the Motor Car Client Worth Index (CPI) was flat for years. That’s not the case and, extra lately, it has risen dramatically together with deductibles. Between January 2019 and July 2024, the typical first-party deductible grew by 47% within the U.S. and 30% in Canada. Drivers with larger deductibles usually make totally different choices with regards to submitting collision-damage claims, which may end in fewer “small”, first-party claims in 2025.

3. Car Complexity is Driving Up Severity

Regardless of fewer claims, common severity for repairable autos elevated by over 5% within the first half of 2024 in comparison with the identical time in 2023. Traditionally, that quantity has risen at a charge nearer to three% or 4%.

A major cause for the expansion in repairable severity is the rise in car complexity. Between 2019 and 2024, the typical variety of alternative components listed on a harm appraisal jumped 15% and these components now characterize greater than 51% of the general restore price. Since 2019, the typical variety of estimate operations has additionally risen by 20%. There are further car parts—together with extra light-weight parts—which have the next alternative charge as effectively. Right this moment it takes extra to return a collision-damaged car to pre-loss situation—extra components, extra operations and extra labor.

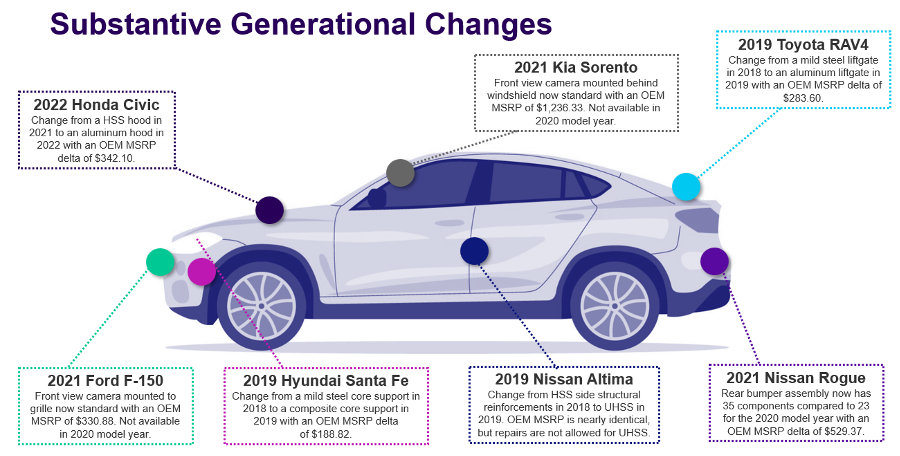

Rising car complexity can also be demonstrated by the totally different supplies utilized in car building. Between 2019 and 2022, extra new physique kinds had been launched than in another interval. These kinds included a rising reliance on the usage of aluminum, composites, particular person components and know-how. A few of that know-how—like entrance cameras—at the moment are normal and require recalibration whatever the collision level of impression and severity. This will enhance the price of restore and create underwriting challenges for insurers.

As autos become old, they’re turning into dearer to restore. In 2024, harm value determinations for the 2019 Toyota RAV4 reveal a rise within the variety of operations (+21%) and components (+11%) in comparison with 2019 value determinations based mostly on Mitchell information—suggesting that the trade’s understanding of repairing these autos has developed. The typical variety of calibrations carried out on a 2019 Toyota RAV4 in 2024 additionally elevated 22%. This isn’t because of a change in accident kind, however a greater understanding of the car’s restore necessities.

Different indicators from 2019 to 2024 that time to severity tendencies persevering with to extend subsequent yr in North America embrace the:

- 27% soar within the common repairable severity for brand new model-year autos

- 50% enhance in common repairable severity for 5-year-old vehicles

- 4% enhance within the frequency of 5-year-old autos

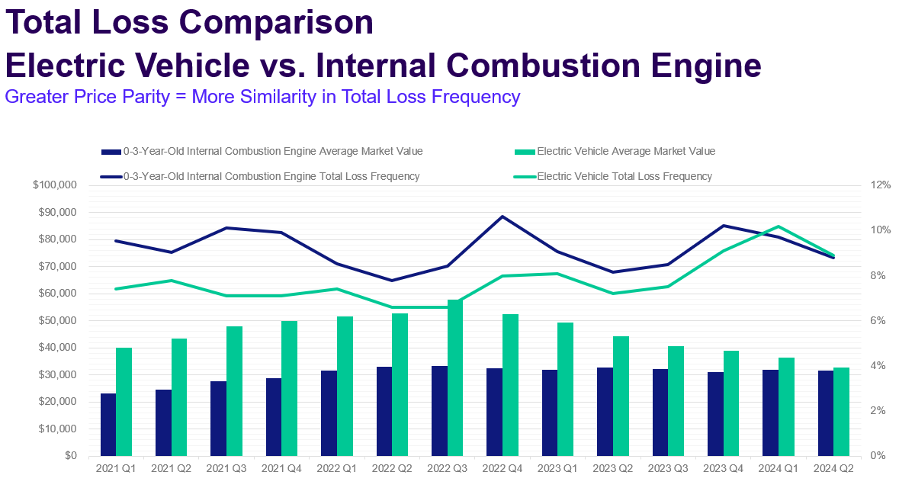

4. Electrical and Hybrid Automobiles Current New Challenges

U.S. battery electrical car (BEV) gross sales grew nearly 52% in 2023 and exceeded the one-million mark for the primary time ever. Though North American gross sales had been comparatively flat in 2024, hybrid gross sales have grown roughly 70% yr over yr. Regardless of the chance that adjustments in U.S. coverage may impression future progress, these ICE options are still expected to increase in market share in 2025.

So why is that important? With regards to declare prices, BEVs are typically dearer to restore than ICE autos because of their complexity. Nevertheless, how far more will depend on the car. Equally, hybrids additionally share most of the similar complexities, however their average claims severity varies based on the type of hybrid. Delicate hybrids—which depend on an ICE as the first propulsion supply—are carefully aligned with ICE autos when it comes to common claims severity. However, plug-in hybrids—which lack an ICE—are practically equivalent to BEVs. BEVs and hybrids even have larger charges of complement submissions following the preliminary harm appraisal—underscoring their added complexity and the elevated must do a tear down of the car to grasp the complete extent of the restore required.

Associated to whole loss outcomes, the tables have turned. With higher value parity between BEV and ICE autos in 2024, whole loss frequencies at the moment are practically equivalent. Final quarter, BEVs totaled at a charge of 9.9% within the U.S. and 10.11% in Canada versus 9.98% and 11.74% respectively for newer ICE vehicles—that are similar to BEVs of their complexity and value to restore. If value parity between the 2 car sorts persists in 2025, count on comparable outcomes in whole loss frequency within the coming yr.

Shifting Gears and Adapting to Change

Based mostly on these tendencies, auto insurers will have to be much more adept at assessing danger and managing prices in 2025—particularly when car developments present no signal of slowing. Nevertheless, by understanding the street forward and enhancing protection choices, loss prevention packages, restore networks, declare workflows and know-how options, carriers can enhance policyholder satisfaction and exceed expectations whereas protecting tempo with future automotive improvements.

Mandell is the director of claims efficiency for Mitchell, an Enlyte firm. He works with insurance coverage executives and materials harm leaders to offer insights and consultative path. He’s additionally the host of the Mitchell Collision Podcast and writer of the corporate’s Plugged-In: EV Collision Insights report.

{kind=link}