Floods

Proposed Flood Zone Growth Would Improve Want for Personal Insurance coverage

Jeff Dunsavage, Senior Analysis Analyst, Triple-I (11/1/2023)

A federal advisory panel’s proposal that the U.S. authorities increase the areas thought of to be at excessive threat of flooding may improve the variety of owners required to purchase flood insurance coverage. Whereas this might improve the quantity of insured flood threat throughout the nation, it additionally may drive up house possession prices and disrupt housing markets.

This potential for disruption will increase the significance of personal insurers changing into extra engaged in underwriting flood protection.

The designated flood zone growth is really helpful by the Technical Mapping Advisory Council, which Congress created in 2012 to strengthen the Nationwide Flood Insurance coverage Program (NFIP). Its members embrace state flood officers and consultants from federal businesses such because the Federal Emergency Administration Company (FEMA) and the Nationwide Oceanic and Atmospheric Administration (NOAA).

Many householders have seen their federal flood insurance coverage premiums rise because of FEMA’s new Risk Rating 2.0 reforms to how NFIP costs flood threat. Ten states and dozens of municipalities are actually suing the Biden administration over the speed hikes.

NFIP has performed a crucial position in filling a safety hole the non-public market was lengthy unwilling or unable to handle. Danger Ranking 2.0 was essential to restore a system during which house owners of low-risk houses successfully backed insurance coverage for house owners of higher-risk ones. On this state of affairs, extra correct pricing was inevitably going to result in elevated charges for some and lowered charges for others. The earlier system was inherently unfair for some and unsustainable for all.

Rising flood insurance coverage charges – mixed with elevated demand for flood protection if the proposed growth takes place – makes it extra vital than ever that personal insurers step in to supply capability.

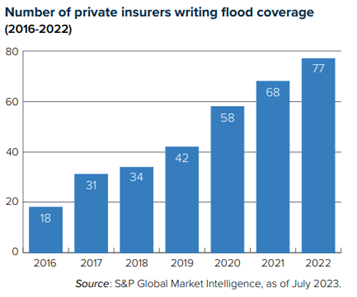

For many years, NFIP was virtually the one supply for flood insurance coverage. The unpredictability of the peril made flood troublesome for the non-public market to insure. In latest a long time, nevertheless, improved knowledge, evaluation, and modeling have helped drive elevated private-sector curiosity in flood. Between 2016 and 2022, the entire flood market grew 24 p.c – from $3.29 billion in direct premiums written to $4.09 billion – with 77 non-public corporations writing 32.1 p.c of the enterprise. That’s a giant change since 2016, when solely 12.6 p.c of protection was written by 18 insurers.

It’s cheap to anticipate that, as the price of collaborating within the government-run flood insurance coverage program rises for some and the dimensions of the market will increase, non-public insurers will acknowledge the chance and reply by making use of cutting-edge knowledge and analytics capabilities, extra refined pricing strategies, and new merchandise, comparable to parametric insurance, to grab these alternatives. It is also incumbent upon communities to discover progressive approaches like community-based catastrophe insurance coverage applications.

Lastly, it’s important for stakeholders to know the significance of any insurance coverage program – non-public, government-run, or some mixture of the 2 – basing its underwriting and pricing on actuarially sound ideas that precisely mirror the chance being transferred.

Wish to know extra concerning the threat disaster and the way insurers are working to handle it? Take a look at Triple-I’s upcoming City Corridor, “Attacking the Risk Crisis,” which will likely be held Nov. 30 in Washington, D.C.

Be taught Extra:

FEMA Names Disaster Resilience Zones, Targeting At-Risk Communities for Investment

More Private Insurers Writing Flood Coverage; Consumer Demand Continues to Lag

Triple-I Issues Brief – Flood: State of the RiskStemming a Rising Tide: How Insurers Can Close the Risk Protection Gap

{kind=link}